Deep-dive AI research reports on individual stocks, powered by our proprietary signals. Every report carries a direction (Bullish or Bearish) and a conviction level(Strong or Speculative). We track stock performance since each report's publication date — because we believe great analysis should be held accountable.

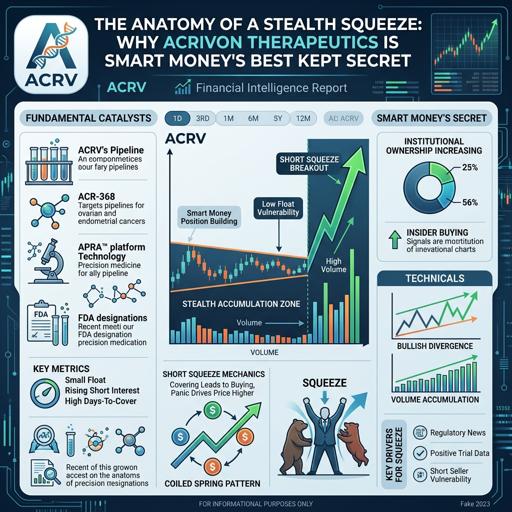

The Anatomy of a Stealth Squeeze: Why Acrivon Therapeutics is Smart Money's Best Kept Secret

Acrivon Therapeutics is a biotech stock showing signs of a major institutional accumulation phase, with management's strategic moves and hidden market data pointing to an imminent, powerful price surge.

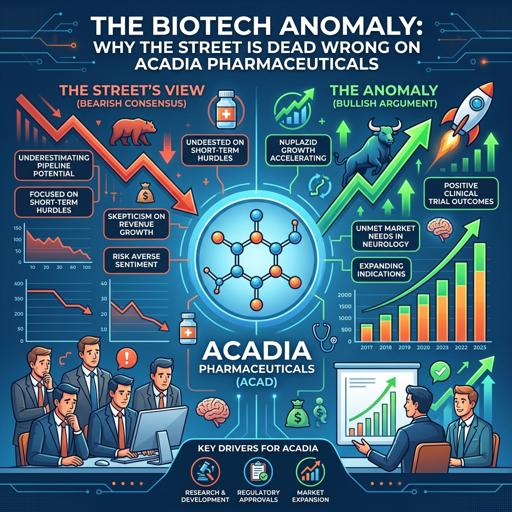

The Biotech Anomaly: Why the Street is Dead Wrong on ACADIA Pharmaceuticals

ACADIA's stock fell despite strong 2025 earnings, $391M net income, and a $1.28B 2026 outlook. Major funds are accumulating shares, and recent trading data signals a powerful reversal is underway.

The Anatomy of a Biotech Shakeout: Why CytomX’s Post-Offering Bleed is a Dark Pool Mirage

CytomX's post-offering stock drop hides major institutional buying in dark pools, signaling a bullish accumulation phase, not a sell-off.

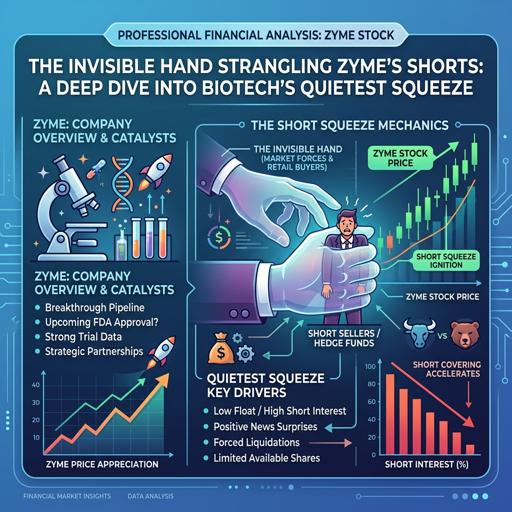

The Invisible Hand Strangling ZYME's Shorts: A Deep Dive into Biotech's Quietest Squeeze

ZYME's stock surge is driven by a hidden institutional squeeze, not just positive news. Data shows massive off-exchange buying overpowering short sellers, forcing a capitulation.

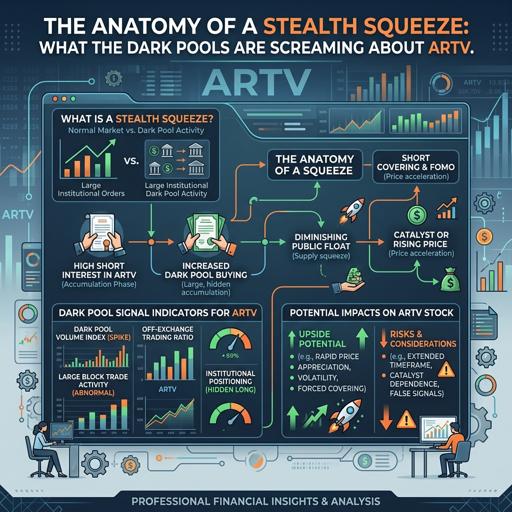

The Anatomy of a Stealth Squeeze: What the Dark Pools Are Screaming About ARTV

Dark pool data suggests ARTV's surge is a smart money-driven repricing, not irrational. Insiders swapped options for stock before a pivotal autoimmune therapy pivot, signaling major upside.

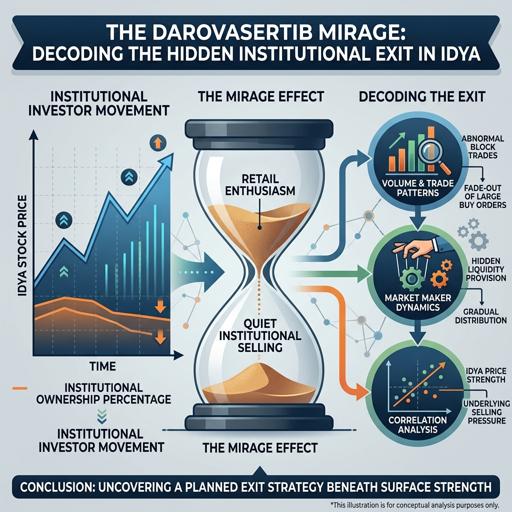

The Darovasertib Mirage: Decoding the Hidden Institutional Exit in IDYA

Institutional investors heavily sold IDYA stock off-exchange after positive trial data, revealing a hidden distribution event despite the public rally.

The $2.25 Billion "Sell The News" Illusion: What Dark Pools Are Hiding in Arbutus Biopharma

Despite a post-settlement price drop, dark pool data reveals aggressive institutional accumulation in Arbutus Biopharma, not selling.

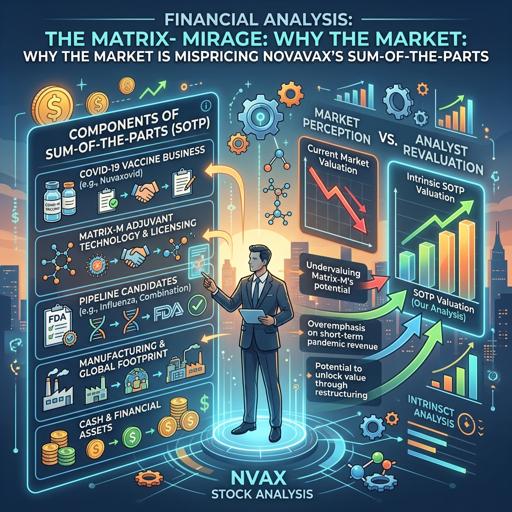

The Matrix-M Mirage: Why the Market is Mispricing Novavax's Sum-of-the-Parts

Novavax is undervalued. It holds $751M cash, has profitable licensing deals for its Matrix-M tech, and faces activist pressure to unlock shareholder value. The market ignores this shift.

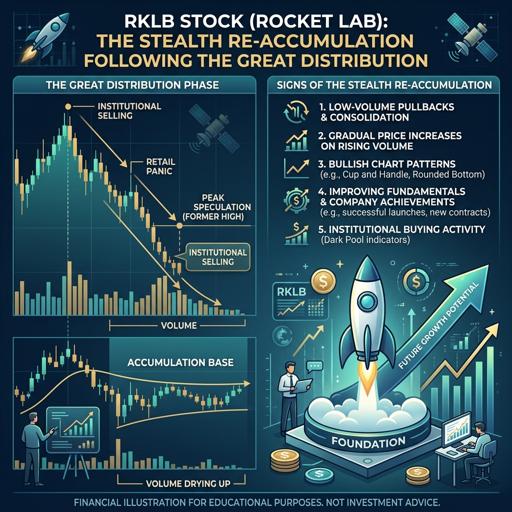

Rocket Lab (RKLB): The Stealth Re-Accumulation Following the Great Distribution

Rocket Lab's stock fell 30% after a planned insider sell-off. The distribution phase is now over, signaling a potential stealth re-accumulation by smart money.

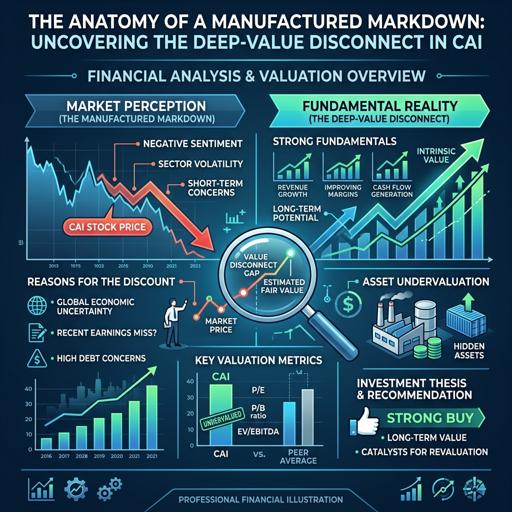

The Anatomy of a Manufactured Markdown: Uncovering the Deep-Value Disconnect in CAI

CAI stock is down 50% despite 97% revenue growth. The plunge is a market illusion, with dark pool data showing heavy institutional accumulation, not a fundamental failure.

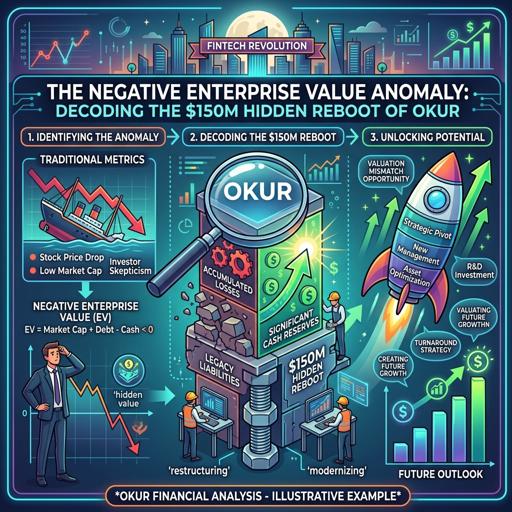

The Negative Enterprise Value Anomaly: Decoding the $150M Hidden Reboot of OKUR

OKUR's stock trades at a negative enterprise value after a $150M private placement. Investors buy the company's IP and cash for less than the cash itself, a deep-value anomaly.

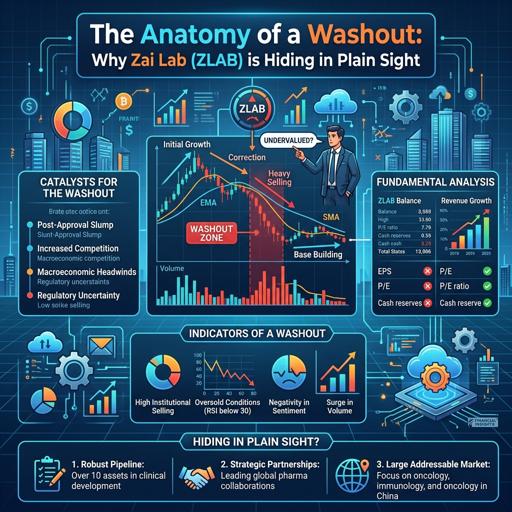

The Anatomy of a Washout: Why Zai Lab (ZLAB) is Hiding in Plain Sight

Zai Lab (ZLAB) crashed to $16.30 in early 2026 due to forced institutional selling. However, sharp hedge fund RA Capital bought a 5.2% stake at the bottom, signaling a major accumulation event hidden in dark pool data.

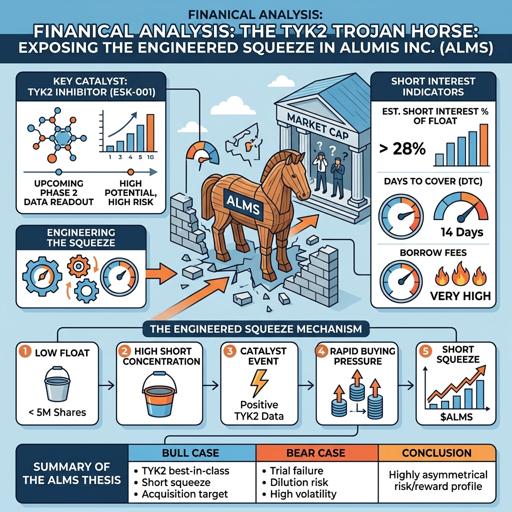

The TYK2 Trojan Horse: Exposing the Engineered Squeeze in Alumis Inc. (ALMS)

Alumis's stock surge is a cynical liquidity event. Insiders bought low, hyped Phase 3 data, then sold shares high in a $345M offering. Despite cash, the drug faces a crowded market and massive cash burn.

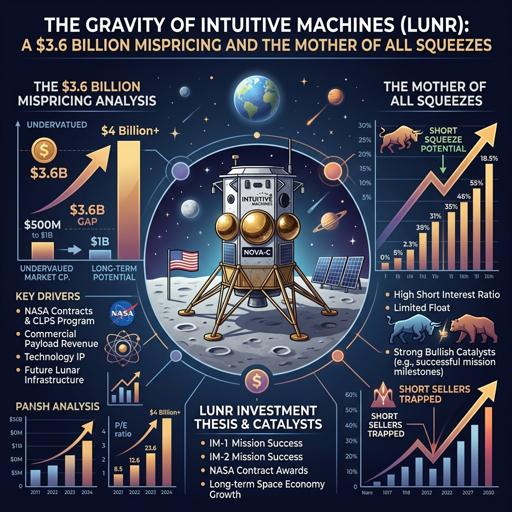

The Gravity of Intuitive Machines (LUNR): A $3.6 Billion Mispricing and the Mother of All Squeezes

LUNR is a mispriced, gov-backed space infrastructure play. Its revenue is set to quintuple in 2026. High short interest and a tiny, locked-up float create a massive squeeze potential.

The $6.7 Billion Mirage: Why Centene's (CNC) Manufactured Crisis is the Ultimate Bear Trap

Centene's $6.7B non-cash impairment triggered a sell-off, but the firm has $17B cash. Sophisticated funds are buying as insiders align for a major stock price recovery.

The Great Robinhood Heist: Buy the Dip Insiders Created

Robinhood stock crashed 55% despite strong fundamentals, as insiders sold millions of shares at peak prices. Now, extreme off-exchange trading signals suggest major institutional accumulation at the $68 level.

The Yoga Pant Paradox: Why Lululemon's Deep Squat is a Generational Buy

Lululemon's stock is down 44% despite strong cash flow & 60% margins. The market overreacted to a US slowdown, ignoring international growth & a $1B buyback. Activist pressure from founder Chip Wilson could unlock value.

The Alchemy of Capital: How Vor Biopharma (VOR) Engineered the Ultimate Wall Street Reset

Vor Biopharma executed a reverse split, insider selling, and major capital raises. This crushed the stock price but secured $450M cash, resetting the company for institutional investors.

The Pickaxes of the AI Gold Rush: Why Target Hospitality (TH) is the Backdoor Data Center Play You Missed

Target Hospitality (TH) pivots from oil to AI infrastructure, securing a $550M+ contract to house data center workers, driving a major stock surge.

The Optical Illusion: Why Ciena’s Parabolic Run is a Trap

Ciena's stock soared 500% on AI hype, but its 440x P/E ratio and exhausted short squeeze signal a dangerous bubble primed for a sharp correction.