Deep-dive AI research reports on individual stocks, powered by our proprietary signals. Every report carries a direction (Bullish or Bearish) and a conviction level(Strong or Speculative). We track stock performance since each report's publication date — because we believe great analysis should be held accountable.

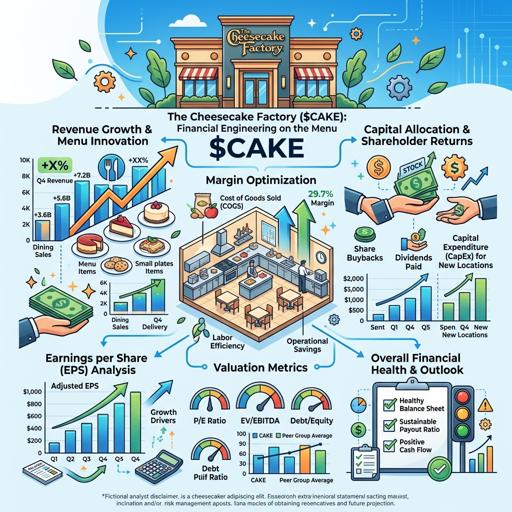

The Cheesecake Factory ($CAKE): Financial Engineering on the Menu

Cheesecake Factory's revenue growth masks a 2.2% same-store sales decline. It's funding dividends and buybacks with new debt while insiders sell, signaling deep financial trouble.

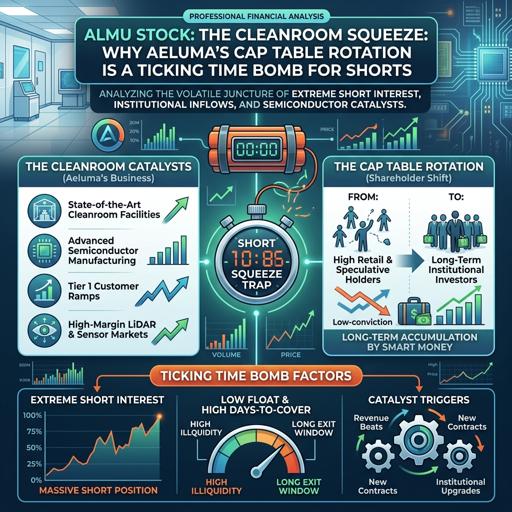

The Cleanroom Squeeze: Why Aeluma’s Cap Table Rotation is a Ticking Time Bomb for Shorts

Aeluma's high short interest is a trap. The company has a strong cash position, and recent insider selling represents a cap table rotation, not a failing business. Bears are misreading the data.

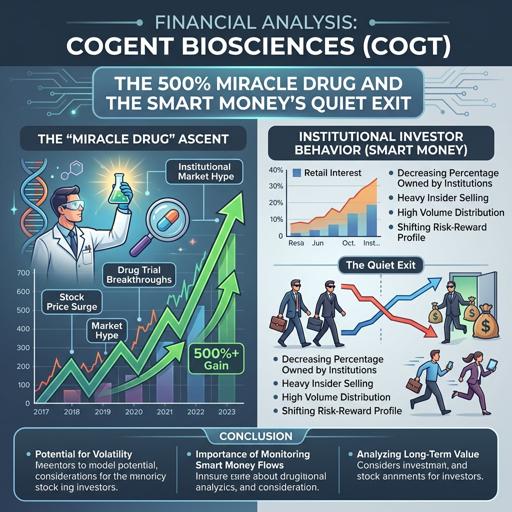

Cogent Biosciences (COGT): The 500% Miracle Drug and the Smart Money's Quiet Exit

Cogent Biosciences' stock surged nearly 500% on strong drug trial data. However, insiders are selling, a large convertible note offering creates a price ceiling, and the stock now prices in perfection, suggesting the rally may be over.

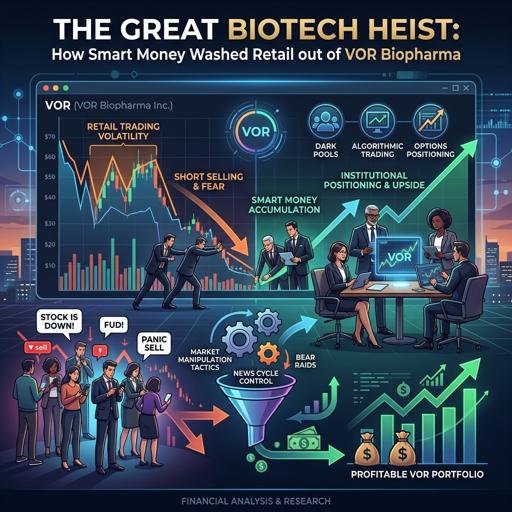

The Great Biotech Heist: How Smart Money Washed Retail out of VOR Biopharma

Smart money orchestrated a VOR Biopharma sell-off, then bought back shares at a 60% discount via a PIPE, recapitalizing the company. Retail was washed out.

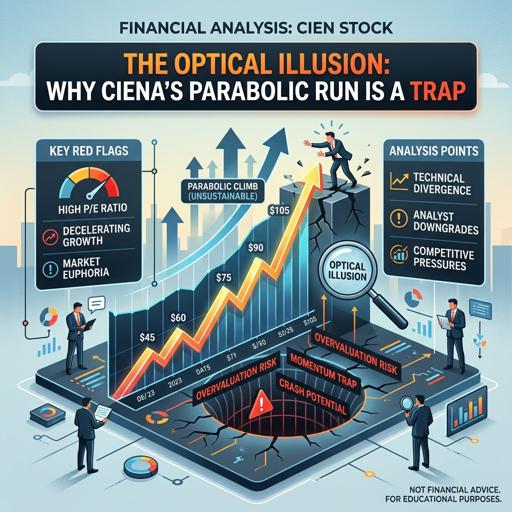

The Optical Illusion: Why Ciena’s Parabolic Run is a Trap

Ciena's stock soared 500% on AI hype, but its 440x P/E ratio and exhausted short squeeze signal a dangerous bubble primed for a sharp correction.

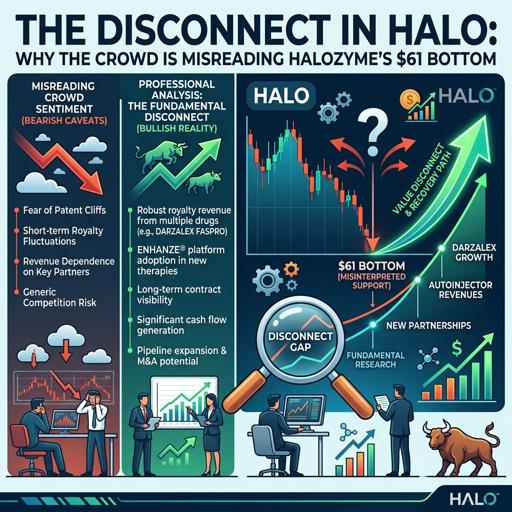

The Disconnect in HALO: Why the Crowd is Misreading Halozyme's $61 Bottom

Halozyme's stock drop is misunderstood. The "institutional selling" is an accounting change, not a real exit. Insider sales are pre-planned for taxes. The CEO's new pay package requires the stock to hit $115 to fully vest, showing strong board confidence.

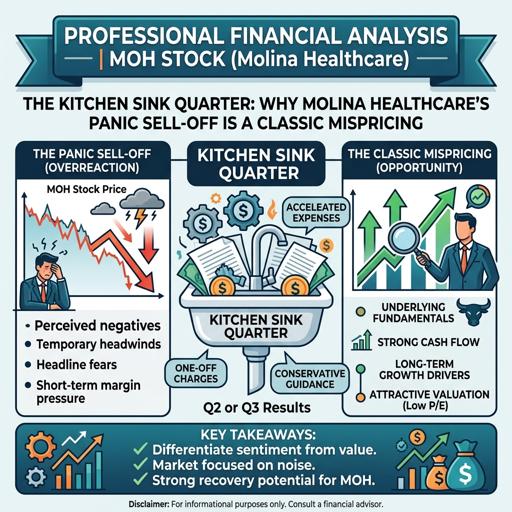

The Kitchen Sink Quarter: Why Molina Healthcare's Panic Sell-Off is a Classic Mispricing

Molina Healthcare's stock plunged after a tough Q4 2025 and weak 2026 guidance. However, the sell-off is a mispricing. Management is taking aggressive, one-time actions to exit a troubled business and reset for a future margin recovery, creating a contrarian opportunity.

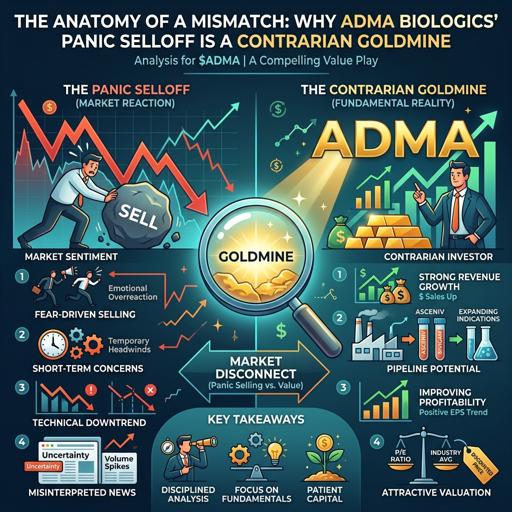

The Anatomy of a Mismatch: Why ADMA Biologics' Panic Selloff is a Contrarian Goldmine

ADMA's panic selloff is a contrarian opportunity. The CEO's stock sales and a misunderstood $125M share buyback triggered the crash, but the company's fundamentals remain strong.

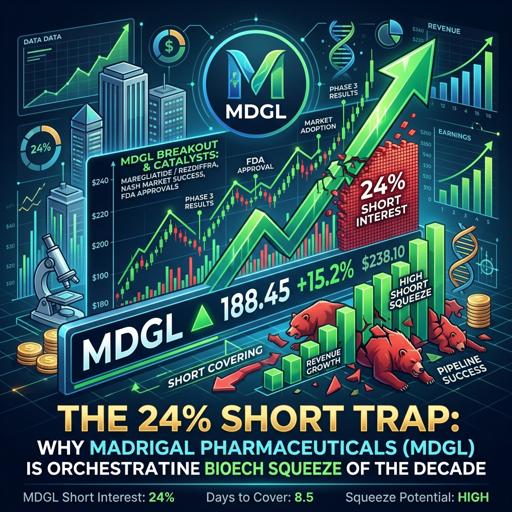

The 24% Short Trap: Why Madrigal Pharmaceuticals (MDGL) is Orchestrating the Biotech Squeeze of the Decade

Madrigal Pharmaceuticals (MDGL) is poised for a major short squeeze. With 24% of shares short, bears are misreading the data. The company has neutralized the GLP-1 threat via a licensing deal, extended key patents to 2045, and is hitting revenue milestones.

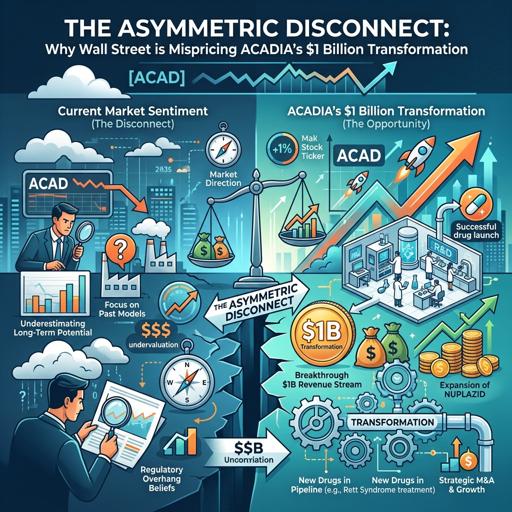

The Asymmetric Disconnect: Why Wall Street is Mispricing ACADIA's $1 Billion Transformation

ACADIA's stock is mispriced. It's a profitable $1B+ revenue company with $820M cash, yet trades low due to misunderstood tax-related insider sales and temporary IRA charges. The market ignores its strong financials and pipeline.

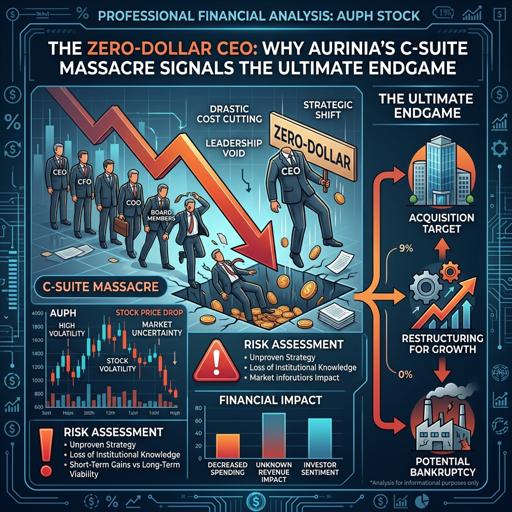

The Zero-Dollar CEO: Why Aurinia’s C-Suite Massacre Signals the Ultimate Endgame

Aurinia's stock surge is just the start. The biotech is now a cash-generating machine with a cheap valuation. A recent boardroom coup by activist Kevin Tang signals a likely sale or major strategic shift is imminent.

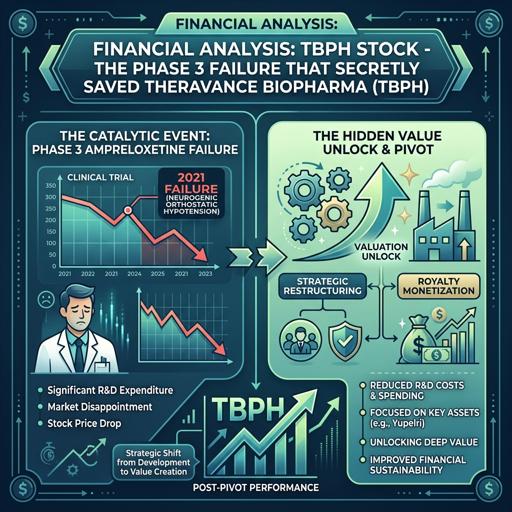

The Phase 3 Failure That Secretly Saved Theravance Biopharma (TBPH)

Theravance Biopharma's stock crashed after a Phase 3 trial failure. However, the company now has a strong cash position, zero debt, and profitable assets like YUPELRI and Trelegy royalties. With R&D costs slashed, it's transitioning to a cash-generating business at a deeply undervalued price.

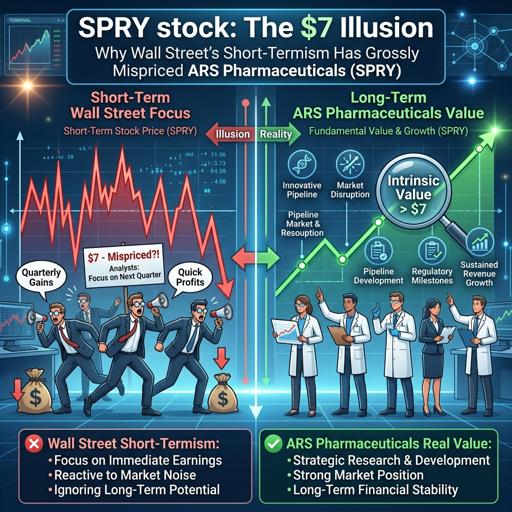

The $7 Illusion: Why Wall Street's Short-Termism Has Grossly Mispriced ARS Pharmaceuticals (SPRY)

Wall Street's short-term focus has mispriced ARS Pharmaceuticals (SPRY). The market is fixated on launch losses, ignoring its strong revenue start, ample cash, and potential to disrupt the multi-billion dollar epinephrine market.

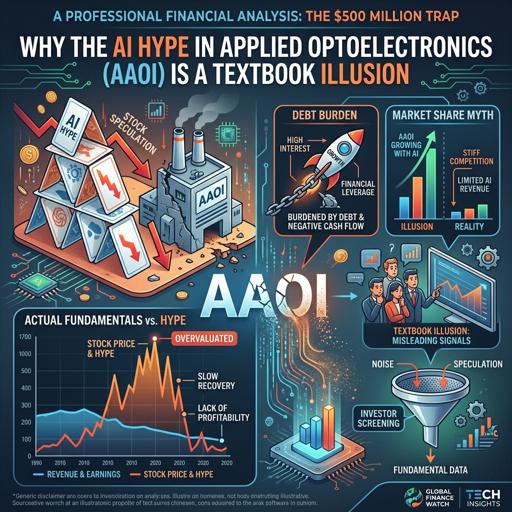

The $500 Million Trap: Why the AI Hype in Applied Optoelectronics (AAOI) is a Textbook Illusion

AAOI's stock surged on AI hype, hitting a $6.5B valuation. However, the company is still losing money despite record revenue, and insiders are aggressively selling their shares.

Priced for Perfection: The $6.5 Billion Question Hanging Over Apogee Therapeutics

Apogee's stock soared 96% on strong trial data, valuing it at $6.5B. However, insiders are aggressively selling shares, signaling major risk for the pre-revenue biotech.

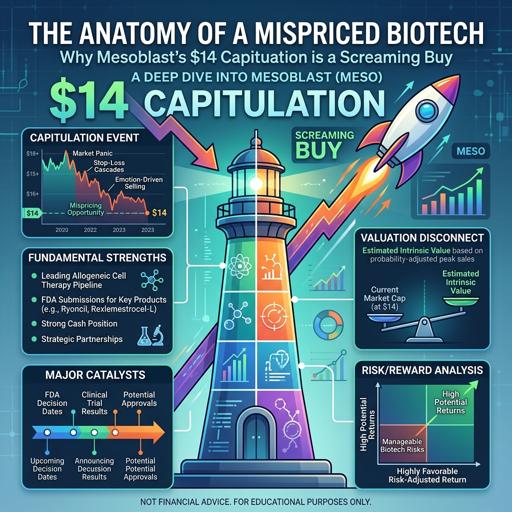

The Anatomy of a Mispriced Biotech: Why Mesoblast’s $14 Capitulation is a Screaming Buy

Mesoblast's $14 stock price is a mispriced opportunity. A key insider bought out toxic debt, provided cheap financing, and invested $16M in shares. The company is now commercial with strong revenue growth, not a speculative cash burn.

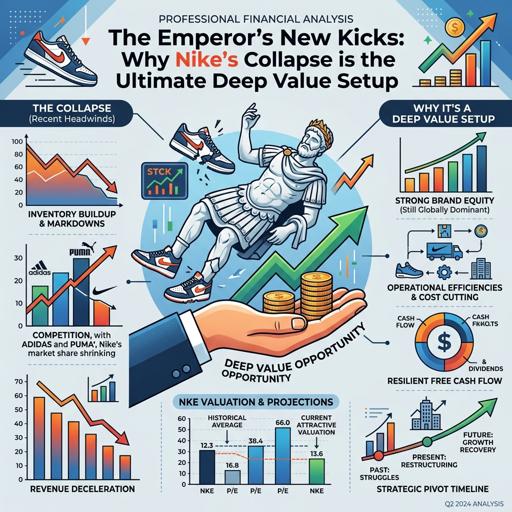

The Emperor's New Kicks: Why Nike's Collapse is the Ultimate Deep Value Setup

Nike's stock collapse is a contrarian deep value setup. The company is undergoing a necessary operational reset, re-engaging wholesale partners to clear inventory and restructuring its leadership for efficiency.

The Disconnect in Phathom Pharmaceuticals: A $16 Wall Street Print Now Trading at an $11 Discount

Phathom stock trades at $11.21, a 30% discount to its $16 January offering price. Despite technical weakness, the firm shows explosive 217% revenue growth and a path to profitability in 2026.

The Anatomy of a Biotech Capitulation: Why Olema Pharmaceuticals (OLMA) is a Mispriced Asymmetry

Olema Pharmaceuticals (OLMA) stock fell 60% on retail panic over insider sales and a CFO departure. However, sophisticated institutions like Fidelity doubled their stakes, buying heavily into the selloff. The company's fundamentals remain strong with a solid cash position.

The $50 Billion Optics Illusion: Why Lumentum's 10x Run is a Siren Song

Lumentum's $50B valuation is inflated by NVIDIA's strategic investment. The deal secures NVIDIA's supply chain, not Lumentum's pricing power. Insiders are selling, signaling the stock's AI optics hype is unsustainable.