Deep-dive AI research reports on individual stocks, powered by our proprietary signals. Every report carries a direction (Bullish or Bearish) and a conviction level(Strong or Speculative). We track stock performance since each report's publication date — because we believe great analysis should be held accountable.

Celcuity Inc. (CELC): An In-Depth Analysis of a Paradigm-Shifting Oncology Asset

Celcuity Inc. (CELC) presents a high-risk, high-reward investment opportunity driven by its lead asset, gedatolisib. This pan-PI3K/mTOR inhibitor demonstrated unprecedented efficacy in the Phase 3 VIKTORIA-1 trial for PIK3CA wild-type HR+/HER2- advanced breast cancer, showing a 76% reduction in progression risk and 7.3-month PFS improvement. The transformative data triggered a stock surge and enabled a strategic $248.7 million capital raise, extending the cash runway through key catalysts. While the IV administration route and single-asset dependency pose significant commercial and clinical risks, the potential for gedatolisib to become a new standard of care in a multi-billion dollar market supports a Speculative Buy recommendation.

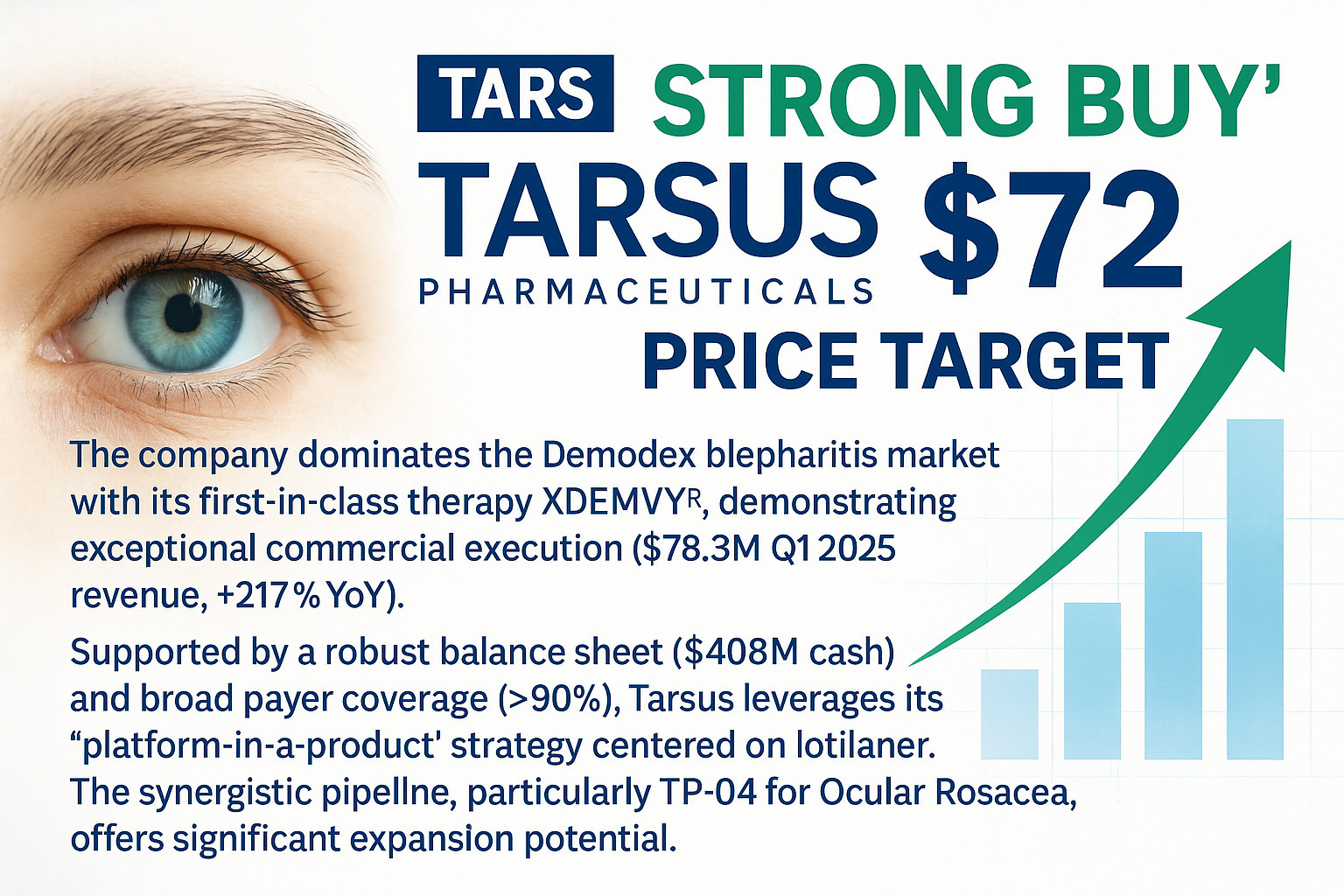

Tarsus Pharmaceuticals (NASDAQ: TARS) - Building a First-in-Class Ophthalmic Franchise

Tarsus Pharmaceuticals (TARS) presents a strong "Buy" opportunity with a $72 price target. The company dominates the Demodex blepharitis market with its first-in-class therapy XDEMVY®, demonstrating exceptional commercial execution ($78.3M Q1 2025 revenue, +217% YoY). Supported by a robust balance sheet ($408M cash) and broad payer coverage (>90%), Tarsus leverages its "platform-in-a-product" strategy centered on lotilaner. The synergistic pipeline, particularly TP-04 for Ocular Rosacea, offers significant expansion potential.

AI Meets Credit: Why Pagaya (PGY) Trades Below Its True Worth

Pagaya Technologies (PGY) presents a compelling buy opportunity at its profitability inflection point. Recent GAAP profitability (Q1 2025), accelerating earnings (preliminary Q2 2025), and a capital-light B2B2C model secured by $5B in forward-flow funding create resilient growth. Despite macroeconomic sensitivity and high volatility, Pagaya trades at a significant discount to peers (e.g., 1.66x P/S vs. Upstart's 9.83x) while demonstrating superior near-term profitability. Initiated with a **BUY** rating and $32.00 price target for 12-18 months.

Hims & Hers Health, Inc. (HIMS): An Investment Analysis of a High-Growth, High-Risk Disruptor

Hims & Hers Health (HIMS) is a high-growth telehealth disruptor leveraging a vertically integrated DTC model to address stigmatized health conditions. It demonstrates explosive revenue growth (111% YoY in Q1 2025), 2.4 million subscribers, and strong profitability. Its "personalization flywheel" – using proprietary data/AI to tailor treatments – drives retention and creates a competitive moat. Expansion into weight loss, menopause, low testosterone, and international markets (via ZAVA acquisition) fuels the bull case. However, existential risks loom: heavy reliance on legally precarious compounded GLP-1 drugs triggered regulatory scrutiny, a severed Novo Nordisk partnership, shareholder lawsuits, and a 30% stock plunge. While operational execution is impressive, severe regulatory/legal overhangs create a binary risk profile. Recommendation: Hold with a $45 price target, reflecting balanced risk/reward amid uncertainty.

VEON Ltd. ($VEON): Banking on Ukraine’s Digital Rebuild

VEON Ltd. (NASDAQ: VEON) presents a high-risk, high-reward opportunity following its strategic exit from Russia and pivot to frontier markets. Trading at a deep discount to intrinsic value, the company offers compelling valuation metrics (forward P/E ~7.8x, EV/EBITDA 3.52x) alongside strong digital revenue growth (+50% YoY) and a transformed balance sheet (net debt/EBITDA 1.23x). Key catalysts include the planned 2025 Nasdaq listing of its Ukrainian crown jewel Kyivstar and potential dividend reinstatement. However, severe geopolitical risks in Ukraine, Pakistan, and Bangladesh, plus structural FX headwinds, warrant caution. Recommended as a Speculative Buy exclusively for investors with high risk tolerance and long-term horizons.

Levi's ($LEVI) is Taking off

Levi Strauss & Co. (NYSE: LEVI) appears attractive at a $25 price target, supported by its ongoing shift to a higher-margin, DTC-led model. Q2 FY 2025 was an inflection point: gross margin reached a record 62.6 %, and EPS of $0.22 beat the $0.13 consensus, powered by DTC revenue rising above 50 % of total sales. Management also authorized an additional $100 million share-repurchase program. Trading at 24.6 × forward P/E with 28 % ROE, the valuation looks reasonable given structurally expanding margins. Key risks: sensitivity to consumer discretionary spending and the inherent cyclicality of fashion trends. Sources Ask ChatGPT

Why KalVista Pharmaceuticals ($KALV) Could Deliver a 3× Return Within a Year

KalVista Pharmaceuticals (KALV) is a biopharmaceutical company whose core asset is EKTERLY®, the first FDA-approved oral, on-demand treatment for HAE. With its convenience, the drug is poised to disrupt the market and is the primary value driver. The company’s oral prophylactic drug in development offers long-term growth potential. Although the company faces risks from commercialization, fierce competition, and financial losses, this analysis views KALV as a high-risk, high-reward investment opportunity and assigns it a "Buy" rating.

Betting on Nebius ($NBIS): The Anatomy of a Potential 10-Bagger

Nebius Group (NBIS) is a high-risk, high-reward AI infrastructure "Neocloud" provider spun out of Yandex. Its investment appeal stems from explosive revenue growth, a strategic partnership granting early access to NVIDIA's latest GPUs, and a strong, debt-free balance sheet. This vertically integrated model promises cost and performance advantages. However, NBIS is currently unprofitable with significant cash burn. It faces fierce competition from tech giants and a direct rival, CoreWeave, while carrying a lofty valuation. Suitable only for long-term investors with high-risk tolerance, the company's success hinges on executing its ambitious expansion and achieving profitability.

CoreWeave-Core Scientific Merger and Its Implication on the Valuation of Iris Energy ($IREN)

The 9 billion CoreWeave−CoreScientific merger validates Bitcoin miners′ strategic pivot to AI infrastructure, establishing power capacity a sakey valuation metric (5-7M/MW). Core Scientific's dependency led to acquisition, while Iris Energy (IREN) pursues independent growth with superior fundamentals: minimal debt, positive cash flow, and industry-leading 15 J/TH mining efficiency. IREN's secured 2.9GW power pipeline dwarfs peers, enabling multi-tenant AI expansion. Sum-of-parts valuation indicates significant undervaluation versus its $4.05B market cap. With 100% renewable-powered infrastructure and proven execution, IREN represents a premier investment for AI infrastructure growth, positioned for organic expansion or strategic acquisition.

Vor Biopharma ($VOR): Putting Every Chip on Telitacicept

Vor Biopharma (NASDAQ: VOR) pivoted from oncology to autoimmunity in June 2025 after near-bankruptcy. The company secured exclusive global rights (excluding China) to RemeGen's Phase 3 drug telitacicept and raised $175 million through a PIPE financing. Post-transaction, VOR focuses solely on advancing telitacicept for generalized myasthenia gravis (gMG), leveraging its strong China Phase 3 data. New CEO Dr. Jean-Paul Kress leads execution. Key risks include massive dilution from 700M+ new warrants, a cash runway extending only to late 2026/early 2027 ahead of pivotal 2027 data, and operational constraints with 8 remaining employees. Prior oncology assets (trem-cel, VCAR33) were discontinued.

Why the SEC Dismantled the Case Against Payment for Order Flow in 2025

Under new Chairman Paul Atkins, the SEC reversed its stance on banning Payment for Order Flow (PFOF) in 2025. The decisive June 12 withdrawal of 14 Gensler-era rule proposals—including the cornerstone Order Competition Rule and Regulation Best Execution—eliminated all pathways to prohibit PFOF. This reflects Atkins' regulatory philosophy emphasizing capital formation, reduced burdens, and market-led solutions over structural intervention. PFOF will remain legal, governed by existing disclosure rules (605/606) and FINRA's best execution standard. The U.S. now diverges from major jurisdictions like the UK and EU that banned PFOF, preserving the zero-commission trading model underpinning retail brokerage economics while maintaining off-exchange execution.

Oscar Health, Inc. (OSCR): An Analysis of a High-Stakes Turnaround Story

Oscar Health (OSCR) presents a high-risk investment opportunity following its recent turnaround to profitability under CEO Mark Bertolini. While demonstrating strong revenue growth (42.2% YoY), improved operational efficiency, and positive cash flow, the insurtech faces existential regulatory risks tied to Affordable Care Act subsidies and policy stability. Despite its innovative technology platform and 2 million members, analyst downgrades, significant insider selling, fierce competition from insurance giants, and extreme stock volatility (Beta 1.90) create "asymmetric downside risk." The stock is suitable only for aggressive, long-term investors tolerant of policy-driven volatility, while conservative investors should avoid due to uncontrollable external threats.

AeroVironment, Inc. (AVAV): An In-Depth Analysis of a High-Stakes Transformation in Defense Technology

AeroVironment is rapidly evolving from a niche drone maker into an all-domain defense-tech leader through its $4.1 billion acquisition of BlueHalo. Surging global defense budgets, demand for autonomous and Counter-UAS systems, and a record $727 million backlog underpin strong long-term growth potential. Yet the deal adds $925 million of debt and will be followed by a $1.35 billion equity/convertible raise, creating dilution and execution risk. Trading near 180× earnings, the stock is priced for flawless integration and sustained double-digit growth. AVAV is a Speculative Buy for risk-tolerant investors, best accumulated on pullbacks.

The Reddit Anomaly: Deconstructing the Drivers of Community-Centric Growth in the Algorithmic Age

Reddit's anomalous growth in the algorithmic social media era stems from its unique community-centric architecture, strategic catalysts, and user migration from mainstream platforms. Its decentralized "community-as-content" model, powered by volunteer moderators and anonymity, generates unparalleled authenticity and niche expertise – a valuable commodity against AI-generated noise. This inherent strength was amplified by winning Google's algorithm through SEO, monetizing data for AI training, modernizing its app/video experience, and its IPO. Simultaneously, user fatigue with invasive data practices, algorithmic feeds, and toxic environments on rivals pushed users toward Reddit's authentic discourse. The critical challenge is balancing aggressive monetization (advertising, data licensing) with sustaining the volunteer communities that create its core value.

Howmet Aerospace (HWM): A Best-in-Class Operator in a Secular Bull Market

Howmet Aerospace (HWM) is positioned as a premier pure-play beneficiary of the commercial aerospace super-cycle, leveraging its technological leadership in mission-critical components. Post-2020 spin-off, the company exhibits exceptional execution: 12% 2024 revenue growth, 480bps EBITDA margin expansion, and $977M free cash flow. Key strengths include dominant market share in non-discretionary engine/airframe components, accelerated high-margin aftermarket growth (17% of revenue), and disciplined capital allocation driving debt reduction (1.4x Net Debt/EBITDA) and buybacks. While secular aerospace tailwinds, defense growth (+15%), and data center-driven IGT demand underpin long-term prospects, the current ~60x P/E valuation poses significant risk. Recommended as a "Buy" for risk-tolerant investors seeking aerospace exposure, with caution for near-term volatility.

Micron Rides the AI Memory Wave—Supercycle Profits Ahead?

Micron Technology (MU) is uniquely positioned to capitalize on the AI-driven memory supercycle. As the sole U.S.-based memory manufacturer, it benefits strategically from government support like the CHIPS Act. Micron’s technological leadership, particularly in high-margin High-Bandwidth Memory (HBM) critical for AI accelerators, is driving a structural shift toward higher, more stable profitability. Strong execution has led to sold-out HBM capacity and record data center revenue, with fiscal 2025 poised for record corporate results. Despite cyclical market risks and intense competition, Micron’s forward valuation appears attractive relative to its enhanced earnings potential. We recommend BUY with a 12-18 month price target of $180.00.

Investment Analysis: Constellation Energy Corporation (NASDAQ: CEG)

Constellation Energy (CEG) dominates U.S. carbon-free energy production (10% national output), leveraging its nuclear fleet and strategic initiatives like the Calpine acquisition and Crane nuclear plant restart to capitalize on surging electricity demand from data centers and EVs. Despite a premium valuation (P/E ~32x vs. industry 18x), its robust operational efficiency (94.6% nuclear capacity), strong financials (upgraded credit rating), and shareholder returns (25% dividend hike) justify a Buy rating for long-term investors. Key risks include regulatory shifts and execution challenges.

Assessment of Robinhood (HOOD) Current Valuation

Robinhood (HOOD) demonstrates strong recovery with $69.28B market cap, driven by diversified revenue (notably crypto +100% YoY), user growth (25.9M funded customers), and improved profitability (P/E 42.42, below historical avg). While regulatory risks (PFOF scrutiny, crypto volatility) and competition persist, its strategic expansion into banking, prediction markets, and international services supports a reasonable valuation for long-term investors.

Can UnitedHealth Group (UNH) Turn around?

UnitedHealth Group (UNH), the largest U.S. health insurer, faces significant headwinds including regulatory scrutiny (CMS V28 rule, DOJ investigations), a major cyberattack impact (~2.9Bcost),andrisingmedicalcosts,causingitsstocktoplummet5025M in shares), UNH presents a compelling long-term BUY opportunity for investors tolerant of near-term regulatory/operational risks.

Investing in China’s Biotech Rise: BeiGene (ONC) and the Future of BeOne Medicines

BeiGene (soon BeOne Medicines) has achieved GAAP profitability in Q1 2025, driven by strong sales of BRUKINSA (792M,+62171M). The company's strategic redomiciliation to Switzerland and recent patent victory bolster its global oncology position. With a robust pipeline (17 Phase 3 trials) and 4.9B−5.3B revenue guidance, BeiGene presents a compelling investment case. Analysts recommend "Buy" given its growth trajectory and profitability.