Deep-dive AI research reports on individual stocks, powered by our proprietary signals. Every report carries a direction (Bullish or Bearish) and a conviction level(Strong or Speculative). We track stock performance since each report's publication date — because we believe great analysis should be held accountable.

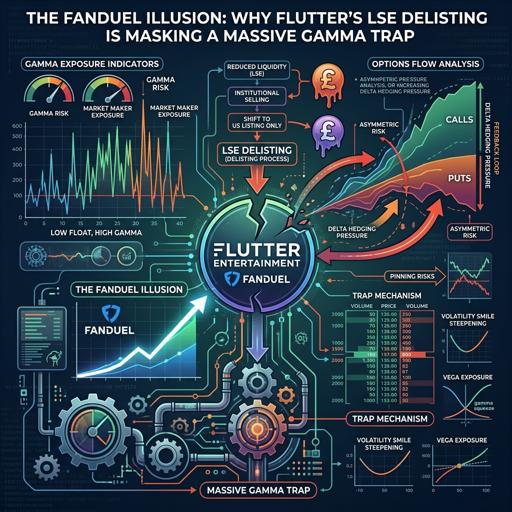

The FanDuel Illusion: Why Flutter's LSE Delisting is Masking a Massive Gamma Trap

Flutter's LSE delisting is forcing European fund selling, while US players accumulate. This creates a severe market dislocation, with options data showing a violent squeeze as bearish bets unwind.

The Hidden Spring in DraftKings: Decoding the Institutional Stealth Bid

Institutional investors are stealthily accumulating DraftKings stock via off-exchange venues, absorbing selling pressure. Options data shows rising positive Gamma, creating a structural floor and setting the stage for a potential upward move.

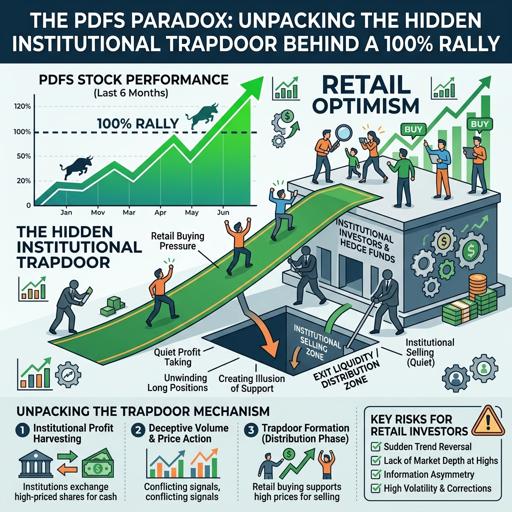

The PDFS Paradox: Unpacking the Hidden Institutional Trapdoor Behind a 100% Rally

PDFS stock's 100% rally masks a major institutional distribution, with dark pool data and options activity signaling an imminent reversal.

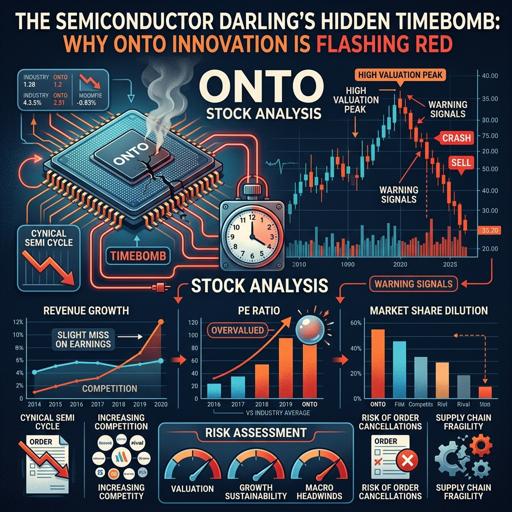

The Semiconductor Darling's Hidden Timebomb: Why Onto Innovation is Flashing Red

Onto Innovation's stock surge is at risk. Institutional investors are secretly shorting shares in dark pools while buying catastrophic put options, indicating a potential sharp price reversal.

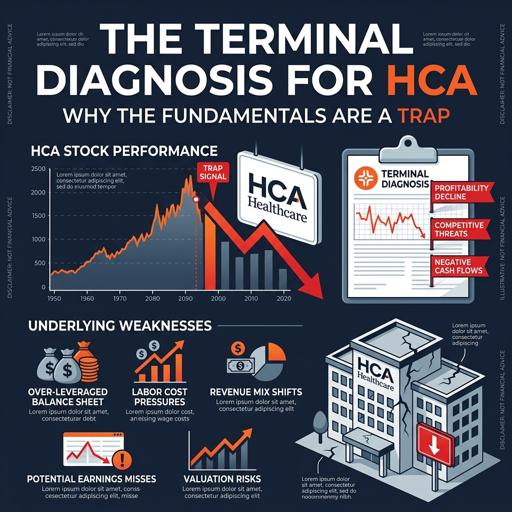

The Terminal Diagnosis for HCA: Why the Fundamentals Are a Trap

HCA's strong fundamentals mask hidden risks. Institutional players are distributing shares to retail via off-exchange shorting, while options data reveals a dangerous gamma trap poised to amplify a sharp downside move.

The AI Mirage: Unpacking the Hidden Gamma Trap in TTM Technologies

TTMI's 430% AI-driven surge masks a hidden gamma trap. Institutional data reveals a sophisticated distribution phase, with off-exchange block selling into retail euphoria, creating a dangerous price-volume divergence.

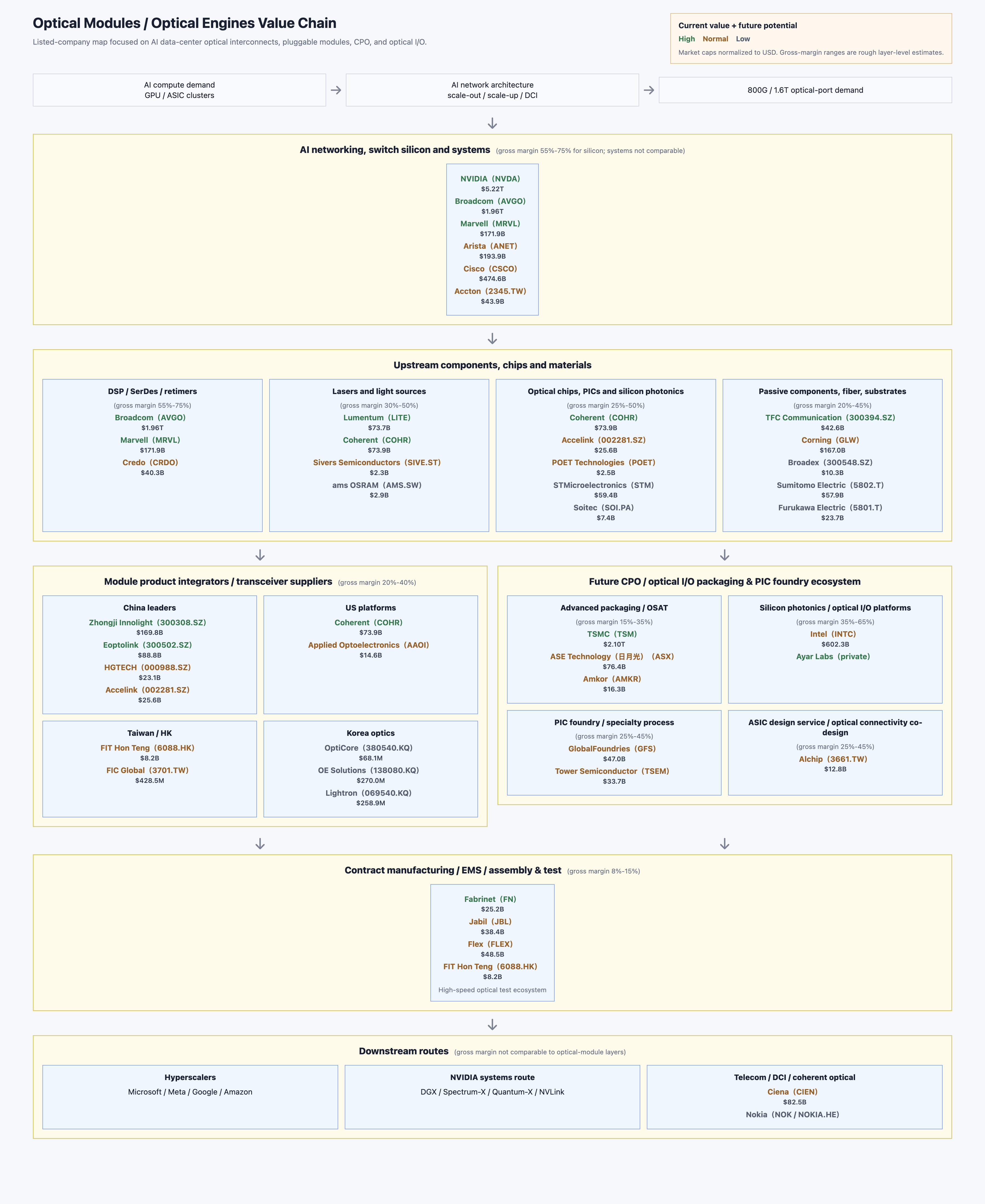

The AI Optics Value Chain: From Switch Silicon to Optical Engines

AI clusters are becoming optical systems as much as compute systems. The visible winner is still the GPU, but the hidden constraint is increasingly the network: switch radix, SerDes speed, optical-port density, power per bit, fiber management, and the ability to move from 800G to 1.6T without letting the interconnect budget explode.

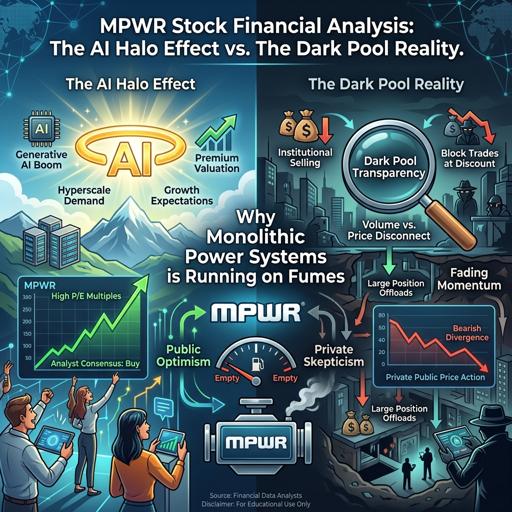

The AI Halo Effect vs. The Dark Pool Reality: Why Monolithic Power Systems is Running on Fumes

MPWR stock surged on AI hype, but executives are massively selling shares. Passive index funds are buying, providing exit liquidity. Hidden market data reveals institutional selling.

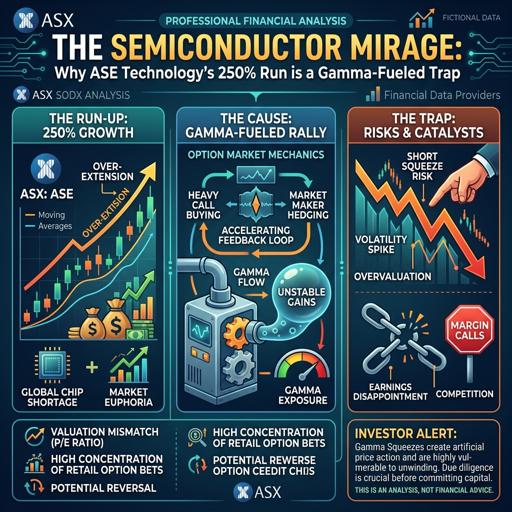

The Semiconductor Mirage: Why ASE Technology's 250% Run is a Gamma-Fueled Trap

ASE Technology's 250% surge is a gamma squeeze, not fundamental growth. Options activity and dark pool data show a synthetic rally, signaling an imminent sharp reversal.

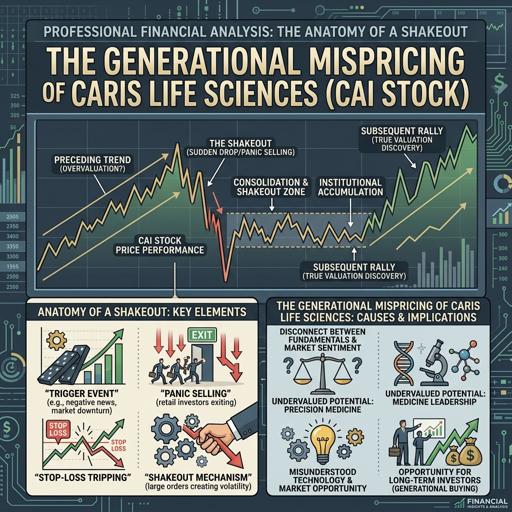

The Anatomy of a Shakeout: The Generational Mispricing of Caris Life Sciences

Caris Life Sciences' stock plunged despite stellar earnings and a $1.2B credit facility. This appears to be a manufactured shakeout, as data shows institutions likely engineering panic to accumulate shares at a generational discount.

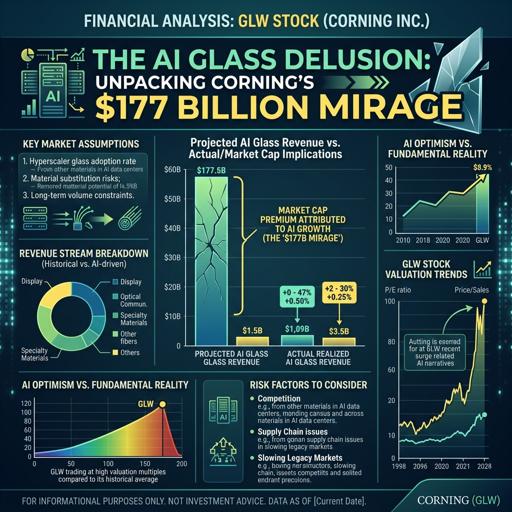

The AI Glass Delusion: Unpacking Corning’s $177 Billion Mirage

Corning's AI-driven stock surge to $177B is a mirage. The NVIDIA deal dilutes shareholders and requires massive capital spending. Insiders are selling, not buying, the hype.

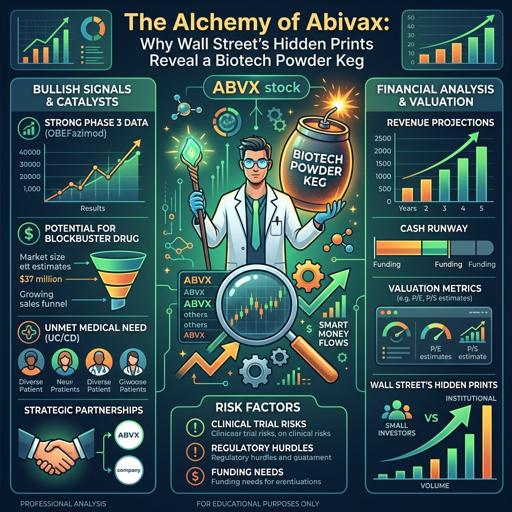

The Alchemy of Abivax: Why Wall Street's Hidden Prints Reveal a Biotech Powder Keg

Abivax is restructuring its balance sheet, buying back royalties with minimal dilution. Its large cash runway and stealth institutional accumulation signal strong potential ahead of key clinical milestones.

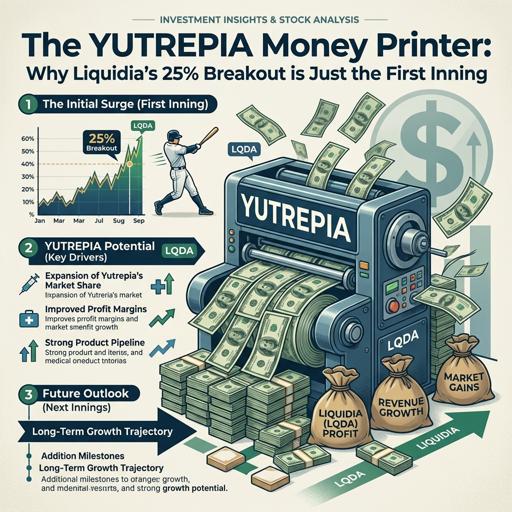

The YUTREPIA Money Printer: Why Liquidia's 25% Breakout is Just the First Inning

Liquidia's 25% breakout is just the start. Q1 2026 shows YUTREIA's $130M sales turned it into a cash-minting machine. Strong institutional buying signals a major structural repricing, not a peak.

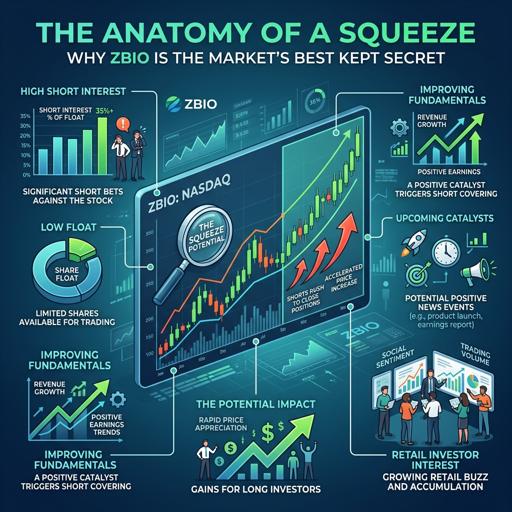

The Anatomy of a Squeeze: Why ZBIO is the Market's Best Kept Secret

ZBIO's recent capital raise funds its key drug launch. Insiders are heavily buying, signaling strong conviction ahead of an imminent FDA submission, while the stock remains undervalued.

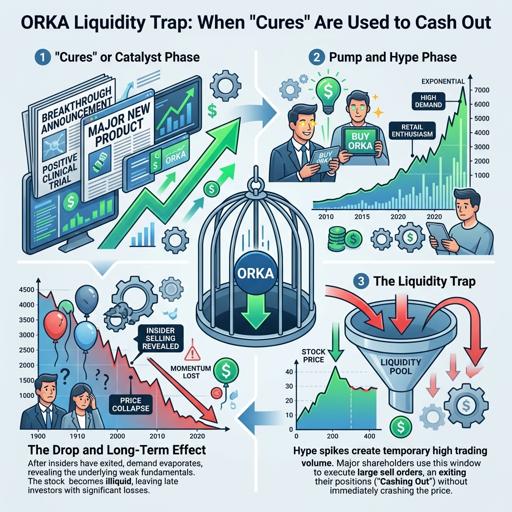

The ORKA Liquidity Trap: When "Cures" Are Used to Cash Out

ORKA's positive trial data triggered a retail surge, but management immediately sold $700M in new shares, causing the stock to plummet. Insiders sold, revealing the data as a liquidity event for a major dilution.

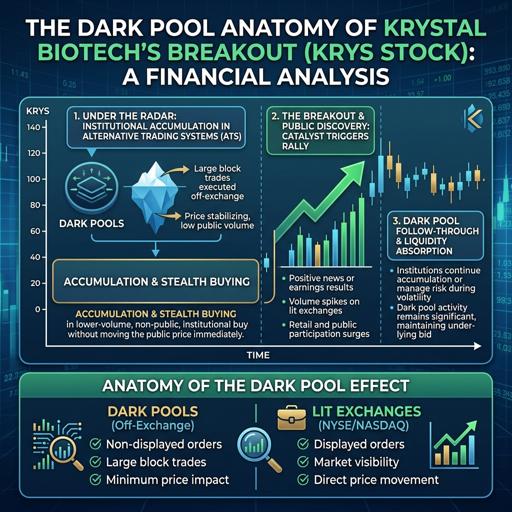

The Dark Pool Anatomy of Krystal Biotech’s Breakout

Krystal Biotech's breakout to $286.95 was driven by institutional dark pool activity, not just strong Q1 2026 earnings. Analysis of off-exchange data reveals a setup of extreme shorting preceding the engineered price move.

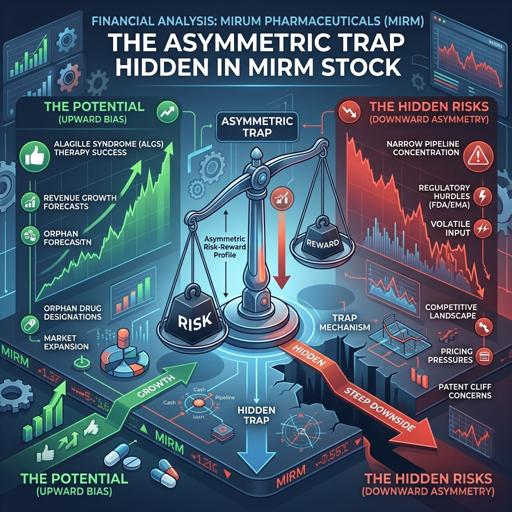

The Asymmetric Trap Hidden in Mirum Pharmaceuticals (MIRM)

Mirum Pharma (MIRM) shows explosive revenue growth and strong cash, yet has 20% short interest. Major funds are accumulating while retail bets on puts, creating a high-tension setup ahead of key positive trial data.

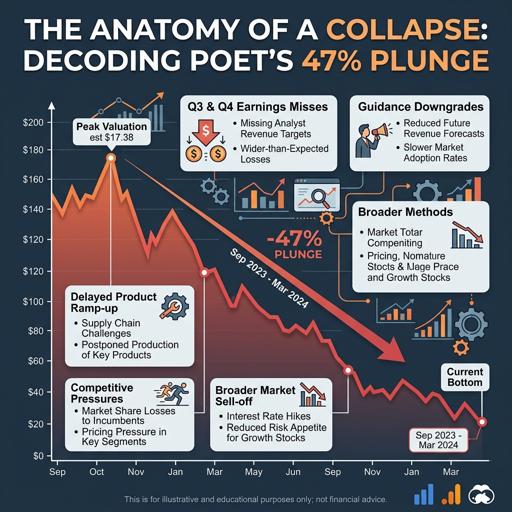

The Anatomy of a Collapse: Decoding POET's 47% Plunge

POET stock plunged 47% after Marvell canceled orders due to POET's confidentiality breach. Options and dark pool data showed institutional investors likely had advance knowledge and were shorting before the public announcement.

The AI Mirage: Why AXTI's 400% Melt-Up is a Ticking Time Bomb

AXTI's 400% AI-driven surge masks unprofitability. Insiders dumped millions in shares as retail bought the narrative, signaling a dangerous disconnect from fundamentals.

The Shadow Accumulation of Prelude Therapeutics: Why The Obvious Dilution is a Trap

Institutional investors, not retail, drove Prelude's recent stock offering. Major funds like OrbiMed increased their stakes, signaling strong confidence in upcoming clinical catalysts despite the apparent dilution.